Scaling NBFC Operations: How AI Voicebots Are Revolutionizing Loan Collections and Slashing OPEX

Points to Remember Before We Get Started:

The Growth Dilemma: NBFCs have been approving loans at unprecedented rates with the help of online onboarding. But, on the flip side, their back-office loan collection operations are incredibly manual, forming a huge bottleneck.

The “Cost to Collect” Catastrophe: Human-based call center solutions for pre-collecting loans significantly boost OPEX owing to employee turnover rates, training expenses, and finite human capabilities.

The Conversational AI Revolution: Unlike old IVRs that would frustrate you to death, today’s advanced AI voicebots are capable of recognizing natural language, negotiating in local dialects, and capturing your intentions precisely.

Conclusion: Innovative financial organizations leveraging AI technology infrastructure have managed to cut down on their Cost to Collect by 40% while increasing their daily outreach tenfold.

The credit market in India is witnessing a significant boom. Non-Banking Financial Companies (NBFCs) and fintech players have become adept at loan disbursement. With the availability of alternative data and smart underwriting algorithms, and even faster e-KYC, a person can easily apply for a personal or business loan and get it directly transferred into their bank accounts within minutes.

The front end of the lending machine is a beautiful specimen of digitalization. But when you look at the backend, particularly the collection department, you’ll find that there is nothing like that.

As soon as the borrower doesn’t pay their EMI, that beautiful digital journey of yours comes screeching to an absolute halt, hitting that wall of manual, highly tedious labor work. In order to collect those payments, almost all NBFCs have big call center floors with people wearing headsets, using Excel sheets to call customers one after another.

It’s time for a comprehensive 1,000+ word blog where we are going to dig deep into the weaknesses of manual call centers in finance, learn about Cost to Collect (CtC), and discover how Conversational AI Voicebots help solve all issues faced by enterprise companies in their NBFCs.

The "Cost to Collect" Crisis: Why Manual Call Centers Fail at Scale

Profitability within the lending sector is highly dependent on a ratio called the Cost to Collect (CTC), which denotes the overall cost that an organization needs to incur in order to collect a delinquent loan.

If your main tool of recovering loans involves human telecalling, then CTC is bound to be high. Here is what makes manual processes silently erode your bottom line:

A. The Limitations of Linearity

While human resources are limited in a linear manner, when one person is able to call 150 clients during his shift, but the number of clients requiring collection services increases tenfold, to 15,000, then the organization needs to employ 100 employees. The company must pay salaries to those 100 people, rent costly commercial premises, buy 100 computers, and obtain software for all of them.

The higher the growth, the higher are the operating costs. In other words, the company is not able to benefit from economies of scale.

B. Unavoidable Attrition in a Call Center

The life of a collection specialist involves constant dealing with stressed clients. As a result, attrition rate for employees working in such conditions is extremely high – it usually exceeds 40%.

If such agents leave after three to four months, the entire expertise that they have gained during their tenure is lost by the NBFC. Thus, the HR department is required to keep spending effort and money on recruitment and training of successive batches of people who end up causing ineffectiveness in the operations of the recovery process.

C. Ineffectively Low Call Connections and Human Fatigue

It is very difficult for manually operated dialers to operate effectively. It can happen that the agent spends considerable time of his day in hearing the ringing tone, busy tone, and answering machine messages. Then once the person does connect, the agent, tired due to being rejected throughout the day, ends up rushing through his conversation.

Conversational AI vs. Legacy IVR: Understanding the Shift

In the context of finance, when professionals think of automated calling, IVRs come to mind. “Press one to make a payment, press two to talk to our executives,” we have all been victims of these archaic interactive voice response systems. These were inflexible, mechanical, and loathed by customers.

The newer Conversational AI Voicebots, however, are nothing like their predecessors. They are powered by the state-of-the-art Large Language Models (LLM) and Natural Language Processing (NLP).

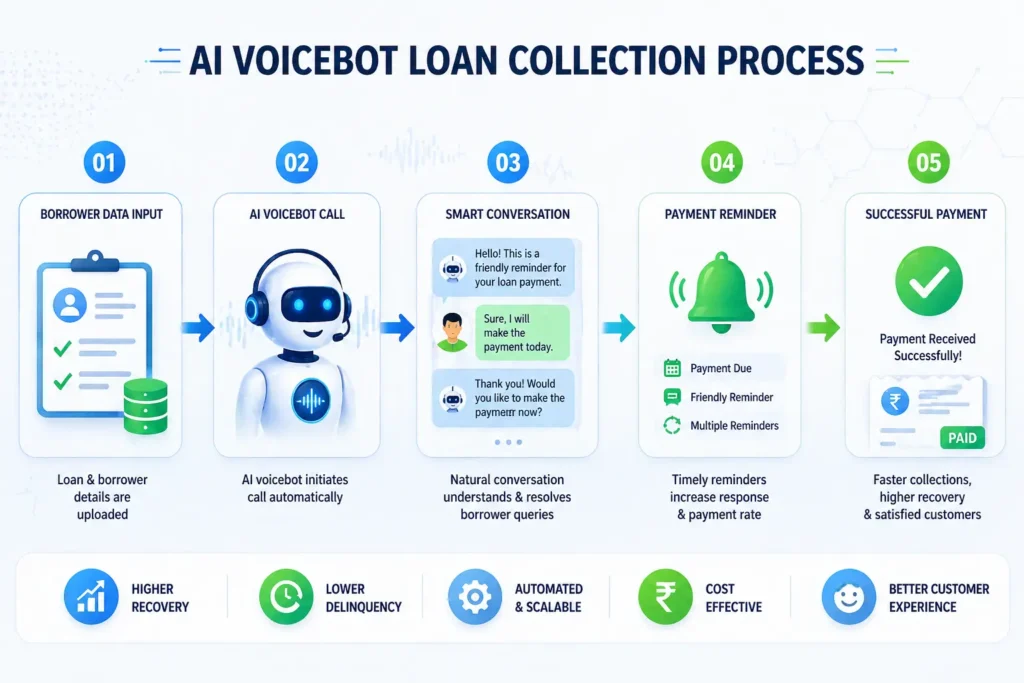

Active Listening: When an AI Voicebot dials up the borrower and announces, “Hi, your EMI of ₹4,000 is due,” and the borrower cuts in, saying, “I have been unemployed since last month, but I promise to make the payment next month,” the voicebot understands and responds with empathy.

Dynamic Negotiation: This technology can be trained to counter any objection. It may accept partial payments or even negotiate a Promise To Pay (PTP) date at a later point during the week.

Vernacular Fluency: For a multilingual country like India, it is important to speak the borrower’s language. An AI Voicebot can switch between Hindi, Marathi, Tamil, Bengali, and English, depending on the geographic location of the borrower.

High-Impact Use Cases for AI Voicebots in NBFCs

Deployment of an AI Voicebot isn’t just replacing the human caller but is essentially rebuilding the whole system with a view to maximizing efficiency. Here are the four most impactful areas in which AI is revolutionizing NBFCs:

1. Pre-Due Date Reminder (The Memory Solution)

There is an overwhelmingly huge number of cases that have defaulted at the earliest stage due to forgetting about the due date. Calling all these people manually through human agents is a sheer wastage of talent. The AI Voicebot has the capacity to call 50,000 borrowers 48 hours before the EMI gets due and remind them to keep their account in ample balance.

2. Bucket 1 & Bucket 2 Collection

When any case becomes overdue between 1-60 days (Bucket 1 & 2) after its payment has failed, time plays a crucial role. The AI Voicebot is programmed to call the client right the next day after the case bounces. In addition, it handles the difficult situation tactfully and finds out the precise reason for the problem and schedules a PTP date.

3. KYC and Follow-Up on Documents

In the loan origination stage, there is usually a delay in processing since a borrower might have submitted a blurry PAN card or forgotten a signature. Rather than having a human operator chase the borrower around for three days, the AI Voicebot will immediately follow up with the borrower on the exact document that needs to be uploaded again.

4. Welcome Calls for Onboarding

Once a loan has been disbursed to the borrower, it would help to make sure that a welcome call is made to check the borrower’s identity and to make sure that the borrower is aware of the repayment plan. This vital step is a high-volume but low-complexity process suitable for AI Voicebots.

The Power of Flawless CRM Integration

The real “magic” of the enterprise-level AI Voicebot is its seamless integration into your core Loan Management System (LMS) or Customer Relationship Manager (CRM) using API webhooks.

In the traditional approach, after completing the call, the agent has to manually input notes into the CRM like, “Customer says they’ll pay on Friday.” This process is prone to typographical errors, incorrect dropdown menu choices, and even failure to document the call.

With the AI Voicebot, data integrity is guaranteed.

After the completion of the conversation, the AI Voicebot automatically analyzes the transcribed text. It identifies the precise date mentioned by the debtor and automatically posts it to your CRM using a webhook.

There’s no manual input involved.

There’s no lag in data updates.

Audit trails are flawless for regulatory purposes.

If the debtor states that they’ll make a payment on Friday, the CRM will be updated immediately. If the payment fails to reach your account by the end of the day Friday, the CRM will automatically schedule the AI Voicebot to conduct the next follow-up call on Saturday morning.

Elevating Your Human Capital

The most common fear in the minds of operational teams is that the introduction of AI will make their human collection agents redundant. This couldn’t be further from the truth. The purpose of AI in your organization is to screen out the noise and enable your people to concentrate on what really matters.

By assigning your AI Voicebot 100% of the task of sending pre-due date reminders, managing routine ‘I forgot’ excuses, and collecting basic data, your human agents will no longer have to endure the ‘auto-dialer’ grind.

The status of your human agents is elevated from rote tasks to that of skilled negotiators. Your people get on the phone to address serious delinquencies (Bucket 3+), manage difficult cases of loan structuring, or handle extremely escalated complaints. By taking away their routine workload, your agents see improved job satisfaction, reduced churn rates, and greater recoveries through their empathetic approach.

Conclusion: The Blueprint for Future-Proof Lending

This industry of credit lending is moving at an insane pace. With non-banking financial companies extending loans to their customers in record numbers, using call centers with a huge number of employees for managing the top-of-funnel collections becomes costly.

In order to generate good profits and to keep your Cost to Collect (CTC) low, while also ensuring that the experience you offer to your customers is professional and multilingual, you have to free yourself from the dependence of your output on your employee count.

With the use of conversational AI voicebots as a layer in your infrastructure, you will be able to scale infinitely, make perfect follow-ups in real-time, and ensure that your CRM data is accurate to 100%.