EMI Reminder Automation for NBFCs: How to Reduce Early-Stage Defaults Using Proactive AI

Points to Note Before Proceeding Further:

The “Forgetful” Borrower: An overwhelming number of defaults from Bucket 1 loans are not caused by any financial stress; rather, they result either from borrowers forgetting their due date or having an insufficient account balance in their bank.

The Human Speed Limit: Human contact centers are incapable of calling their way through several thousands of defaulters within a two-day window before the deduction of EMIs.

Proactivity Works: By automating conversational EMI reminders using Voicebots, millions can be saved by NBFCs down the line from technical failures.

Once the loan moves into Bucket 2 or Bucket 3 (30 to 90+ days overdue), things become complicated; heavy negotiations, legal actions, and strong human intervention come into play. Yet the true battlefield lies in Bucket 1 (1 to 30 days overdue) and the critical period just before the EMI payment date.

The problem starts when the borrower fails to pay via NACH/e-mandate on the 5th day of the month, resulting in penalty on behalf of the NBFC, damage to the credit score of the borrower, and finally making it a case of collections. The conventional approach of having manual calling teams make borrowers aware of maintaining sufficient money in their accounts doesn’t seem to be working anymore.

The Psychology of the Bucket 1 Default

In the event of an EMI bounce, the initial reaction of a collections officer would be to consider that the borrower has run out of money. Although this problem does exist in many cases, when one analyses the larger picture within the context of the BFSI industry in India, it is rather shocking what comes up.

The majority of defaults, referred to by the BFSI sector as ‘Technical Bounces,’ are in fact just that: technical bounces. The borrower has plenty of money. They want to pay off their loans. They do not wish to be called by the collectors or face a bad credit rating. Yet, why did the payments bounce? Simply because they forgot.

Life in today’s world is hectic. With stressful work environments, family pressures, travel, and endless alerts from technological devices, the cognitive capacity of the average individual is overloaded. It is easy for that individual to forget transferring ₹12,500 from their payroll account to the particular bank account that corresponds with the mandate of their loan up until 11:59 PM of the 4th day of the month. There is no need to use strong-arm methods here. Just give them a reminder in a polite manner.

The Bottleneck of Manual Reminders

Where forgetfulness is the issue, then obviously the answer would be reminding them. However, when implementing such a strategy on a countrywide level, one would realize how traditional NBFC functioning fails in its execution.

Now let us look into the math behind a call center that works manually. Suppose your NBFC has 50,000 retail loans due by the 5th of the month. The most opportune time for you to contact these customers would be the 3rd and 4th. You now have a span of 48 hours within which you have to make all these contacts. An average skilled tele caller will be able to make about 150 calls in a day’s work.

It results in huge operational friction:

The Cost: Recruitment, training, and paying salaries to hundreds of agents for just reading out a 30-second reminder message is outrageous and totally uncalled-for Operational Expenditure (OPEX).

SMS Disadvantage: Rather than making the call, most NBFCs depend on automated SMS blasts. The problem with SMS is that it’s a passive channel. In a time where everyone is bombarded with promotional spam, it is quite common for SMS to be ignored.

The Proactive AI Voicebot Solution

The most intelligent financial organizations know not to wait around for that bounce. They know that Proactive AI > Reactive Collections. They are employing Conversational AI Voicebots, created by companies such as Archiz Solutions, to completely automate the pre-due date outreach process.

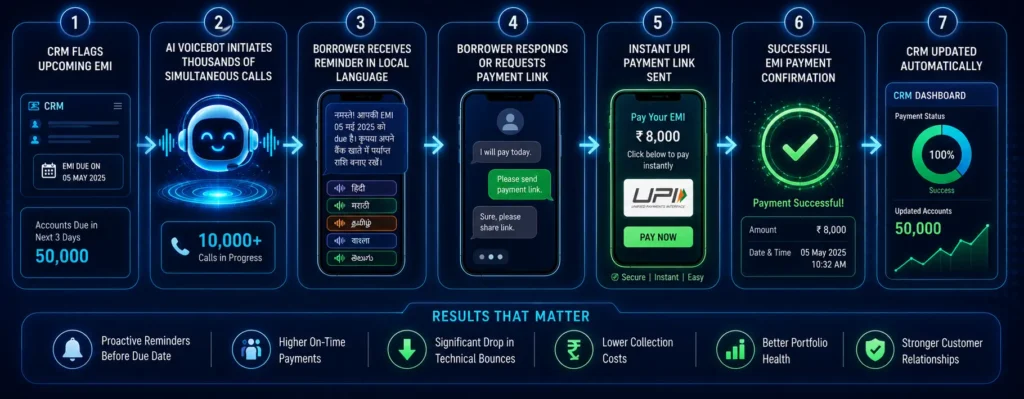

Preemptive CRM Trigger

The LOS or CRM flags the 50,000 accounts that need to be contacted before their due date through the use of API webhooks. This information is automatically forwarded to the AI Voicebot platform.

Infinite Simultaneous Calling

The AI does not call linearly. Rather, it can place up to 10,000 calls at once. It scales elastically, allowing it to accommodate for sudden increases in volume at month-end. It guarantees 100% outreach to your entire client list in a few short hours.

Vernacular and Polite Talk

As soon as the borrower picks up, the AI speaks to him/her in a conversational manner using their local language/dialect. “Hi [Name], this is a friendly reminder call from [NBFC Name]. As per your loan details, an EMI amounting to ₹8,000 is going to be debited on the 5th of this month. Please maintain enough funds in your respective bank account so that the deduction doesn’t bounce and you incur any charges. Hope you are doing well.”

Dealing with the “I’ve Forgotten It” Excuse

In case the borrower says, “Hey I totally forgot it. I don’t have any money there. Can I pay in cash?”, the AI says, “Sure thing. Right away I’m sending a UPI link to this number which will help you pay your dues.

Conclusion: Don’t Wait for the Defaulter