Breaking the "Pending KYC" Bottleneck: How NBFCs Can Automate Customer Follow-Ups Using AI

Points to Remember Prior to Getting into Detail:

Origination Paradox – Even if digital lending algorithms approve loans in minutes, disbursement of such loans can be delayed by days due to missing documents.

Manually Chasing Bottleneck – The burden of manually chasing borrowers to get their KYC done through back-office operations team is huge.

Abandonment Risk – Due to friction while submitting documents, nearly 40% of the applicants who were conditionally approved end up dropping off.

With today’s world of NBFCs and lending startups, the competition for acquiring clients is at its peak. With the use of your advanced underwriting technologies, the borrower is instantly assessed as a potential client and provisionally approved within seconds. The money is waiting to be invested.

But then comes the point when the system comes to a halt because of the “Pending KYC” Status.

The customer attached an image of the blurry PAN card. Or maybe missed signing the final page of the bank statement. At this moment the application becomes a hostage in the hands of paperwork. In case if your firm utilizes an inefficient manual operations department to find the particular client and fix the document issue, you are losing money.

The Anatomy of a Delayed Disbursal

Once the application is identified as being in need of missing, wrong, or invalid documentation, an actual human agent is tasked to handle this problem. Why this is a terrible approach is illustrated in the following ways:

The Never-Ending Phone Tag Game

The operational agent will start off by calling the customer at 11:00 AM. But since it is not possible for the borrower to leave their job just to answer a call, the operational agent will have to record a voicemail message which will be updated in the customer relationship management software as ‘Call Not Answered’. After a few days, once the two connect on the phone, the borrower’s motivation level is already zero.

The High Levels of Drop-Off Rate in Digital Lending

As mentioned earlier, when dealing with digital lending, friction is a killer. If the borrower has to go through the hassle of answering calls from human agents just to verify their documents, the chances of dropping out of the whole process become very high. According to industry reports, between 30% to 40% of conditionally approved applications are abandoned simply due to friction.

Enter the AI Voicebot: Automating the Document Chase

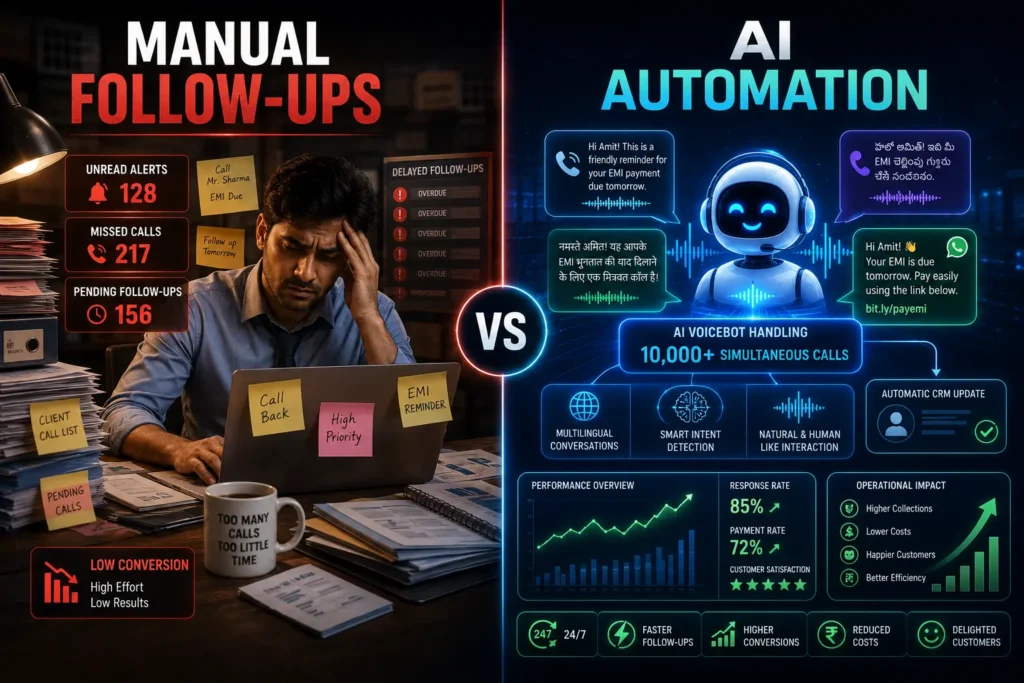

These NBFCs which have the capacity to grow extremely quickly and aggressively are getting rid of the ‘human element’ from this process altogether by introducing Conversational AI Voicebots to function as perfect automated teams for collecting documents.

The following is how the automated AI Voicebot for KYC and document collection works in real-time practice:

The Immediate LOS Trigger

As soon as your system flags the presence of any issues such as blurring, missing, or invalid documentation, your Loan Origination System sends off a trigger through an API webhook to your Voicebot.

The Automated and Personalized Phone Call

A few minutes later, the phone starts ringing on the other side and an automated call comes in. The caller identifies himself by name and addresses the client in his regional language (Hindi, English, Marathi, Tamil).

“Hello Mr. Sharma, this is an automated call from NBFC Name

You have almost filled up your application form for the personal loan! But the image of your PAN card was not very clear. Please kindly share the image again so that we may be able to process your money instantly!”

Omnichannel Link Sharing

The AI makes the process easier by itself. Without ending the call, it continues to say, “Here is the link for uploading the image on your phone through SMS & WhatsApp. Kindly follow it!” Step 4: Real-time Updates and Handling Objections

In case he responds with, “Sorry, I am busy with my work at the office.

I will do it later on in the evening time,” the AI gets his meaning perfectly. It says thank you, sets the scheduled call at 7:00 PM and notes the above statement in his CRM. There is no need of typing anything manually!

Conclusion: Stop Chasing, Start Disbursing

As soon as there is a detection of document errors, through automation the process becomes instantaneous, instead of taking days. The borrower receives the message during his ‘buying frame of mind,’ thereby enabling instant re-uploads and fast approvals of loans.

The future of NBFCs would be through the use of automation and intelligent follow ups. The time has come for implementing the AI voicebot, to break the onboarding bottleneck and create an infinite loan disbursal pipeline.