5 Ways AI Voicebots Are Transforming NBFC Operations: A Complete Awareness Guide

However, when the financial leadership talks about the role of Artificial Intelligence in the Non-Banking Financial Company (NBFC) space, they automatically get to back office-related use cases. Risk management analysis, predictive algorithms, and credit underwriting through algorithms are some common examples.

Undoubtedly, such applications of AI are extremely powerful, but there is another area of Artificial Intelligence that has the power to impact daily operational efficiency, customer experience, and ultimately revenue – Conversational AI Voicebots.

In the past few decades, NBFCs and FinTech companies used a large manual workforce for handling calls related to sales, collections, document verification, and customer support. In all the cases, a person had to manually make calls through dialing a 10-digit telephone number. But as more and more customers join the database, the traditional way of managing calls does not hold any value anymore. It is too slow, too error-prone, and costly.

AI Voicebots have become far more intelligent and flexible than the old-fashioned “Press 1 for English, Press 2 to speak to an executive” IVR systems that customers dislike universally. These modern voicebots employ powerful natural language processing and large language models. They are very intelligent and highly natural and form integral components in infrastructure used by almost every department at a financial institution.

As an NBFC Founder, CTO, or Head of Operations, it’s vital that you create awareness about this technology to ensure survival in a highly competitive industry. Here’s everything you need to know about the various uses of AI Voicebots across the entire lending journey.

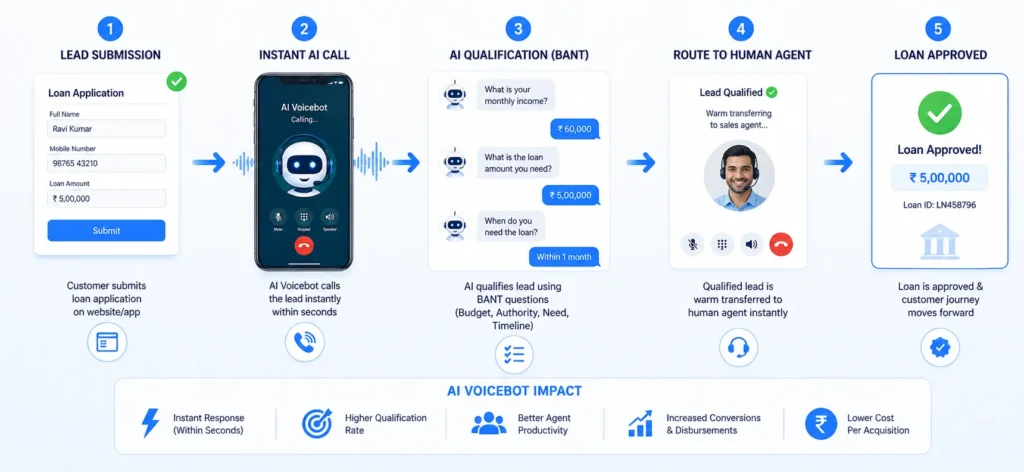

Instant Lead Qualification (Speed to Lead)

Problem Statement: Your marketing department creates highly optimized ads on Facebook and Google that result in dozens of leads every day. The CPL is fantastic. Yet, humans working in sales can be too busy, away from work, or simply swamped with the lead volume.

Responses usually take hours, sometimes even days. In today’s competitive lending environment, the modern consumer does not have any patience at all. If the person fills out a form to get a loan, and if you do not call them within 5 minutes, they are going to switch tabs and fill out a form with your competitor.

Voicebot Solution: The AI Voicebot eliminates the “Speed to Lead” bottleneck entirely. From the moment that the potential client hits submit on their application form on your website, the webhook activates the AI Voicebot to dial out.

Qualification Process: The AI speaks conversationally and qualifies your prospects using BANT (Budget, Authority, Need, Timeline). It asks such questions as “What is your monthly income?”, “Are you in need of a secured or unsecured loan?”, and “What is the required loan amount?”

Seamless Connection: When your prospect qualifies according to your unique underwriting standards, then your AI will automatically warm connect them with a human sales agent right away. However, if it happens to be after working hours, your AI will automatically schedule an appointment for the following morning.

The Result: No marketing money wasted, virtually zero response time, and high-quality pipeline leads for your sales agents. There is no more wasting valuable energy calling one hundred people to discover five prospects for your sales agents to talk to.

Frictionless KYC & Document Follow-Ups

The Problem: A borrower makes an application for a loan which gets conditionally approved based on your algorithm but suddenly gets stalled due to either a blurred picture of their PAN card or missing signature from their bank statement of the past six months. The application thus gets stuck in “Pending KYC.” Relying on human operations staff for reaching out to the customer and informing them about document issues is time-consuming and tedious. And all this results in an app rejection rate of 40%.

The Voicebot Solution: Rather than a human agent reaching out manually after leaving countless voicemail messages, you use the LOS to trigger an AI-powered Voicebot call to the customer.

Instant Notifications: The bot dials the customer and courteously explains which specific document is lacking or wrong.

Actionable Links: At the time of the phone call, the bot sends out a one-click notification via SMS or WhatsApp that leads to a secure site where the customer can immediately capture the new image of the document.

The Results: Dramatic improvement in TAT of loan disbursements. Solving the onboarding bottleneck problem right away translates into a huge drop in abandoned applications, which in turn means that stuck applications will now become disbursed and revenue-generating loans.

Automated EMI Reminders & Early-Stage Collections

Problem Statement: While financial trouble is the most cited reason for Bucket 1 collections, which happen during the early stage of loan defaults, the main problem lies with human forgetfulness. People forget about their EMI due date among all the things they have going on in life. Utilizing highly paid humans to dial up customers like robo callers to inform them that, “Your EMI is due tomorrow,” is a costly, dehumanizing, and highly inefficient process.

Voicebot: It could be said that this is one of the most lucrative use cases for Voice AI within the finance industry.

Proactive Calls: Two days prior to the due date, the Voicebot proactively dials the borrowers and politely informs them about the amount and asks them to ensure they have adequate funds in their bank accounts to save themselves from any bounce fees.

Intent Detection: In case there is a bounced payment, the voicebot contacts the defaulter. If he/she makes some excuse, saying something like, “I haven’t gotten my salary yet. I will pay off by Friday evening,” the voicebot perfectly recognizes the natural language. Not arguing with the customer at all, the bot acknowledges the answer and adds the PTP date into the CRM database.

Impact: The cost of operational calls has been reduced by 40%. Moreover, since the AI is guaranteed to reach all borrowers 100% effectively without any weariness, the NBFCs have a much better repayment ratio.

24/7 Routine Customer Support

The Problem: Over 70% of all the calls that reach the customer care center of the NBFC are repetitive in nature. They include inquiries like “What is my loan balance?”; “Do I get a NOC?” and “When do I pay my next EMI?”. Making the customer go through waiting for 15 minutes to receive such one line answers makes them lose faith in your brand.

The Voicebot Solution: The voice bot acts as the perfect digital receptionist.

Instant Answers: When the customer calls, the voice bot instantly verifies his/her identity using either of the two ways – OTP or by verifying the customer’s registered mobile number. Next, it pulls up the data from the core banking systems/LMS and tells the customer about it.

Smart Routing: In case a consumer has a complicated issue, a fraud case, or seeks restructuring of his/her loan, the AI system detects the complicated emotions and immediately directs the call to the dedicated human representative.

Benefits: No wait times for consumers and enormous cost savings on staffing at the call center. Your human representatives can now fully focus on solving problems, significantly enhancing job satisfaction and customer service.

Vernacular Outreach for Tier 2 & Tier 3 Markets

The Problem: The next big boom for digital lending will come from “Bharat” – India’s Tier 2, Tier 3, and Tier 4 cities. But, as NBFCs rapidly grow their portfolios in these regional areas, they encounter an insurmountable language problem. A borrower in rural Tamil Nadu or Maharashtra wants to speak in his native tongue. Setting up and maintaining a huge multilingual BPO call center in an urban area is logistically and financially unfeasible.

The Voicebot Solution: The AI Voicebot has a superpower that humans lack – the ability to be instantly fluent in multiple languages.

Dynamic Language Selection: Using the pin code of the borrower, customer information from the CRM, or the spoken language itself, the AI voicebot can seamlessly switch between languages like Hindi, Marathi, Bengali, Tamil, Telugu, Kannada, Gujarati, and many others.

Cultural Empathy: Since the bot communicates fluently in the language that is spoken at home, the borrower is shown respect. Communication makes one trustworthy in the finance industry, and since the trust levels improve instantly, it is essential for obtaining payments and brand loyalty from the regions concerned.

The Outcome: Expansion into new territories without having to worry about recruiting linguistic talent with human resources. The company does not have to recruit new AI for lending operations in all parts of India.

Conclusion: Stop Dialing, Start Automating

The age of sprawling call centers for telemarketing purposes in the banking sector is drawing its last breath soon. The traditional linear business model wherein you have to hire 10 additional salespeople whenever there is a 10% rise in your loan portfolio cannot survive in a competitive environment.

With the incorporation of AI Voicebots as an essential component of your technology stack, instead of just a fancy toy, you can completely restructure your NBFC business model.

Starting from when the customer lands at your doorstep, then moving onto smooth and seamless KYC, all the way till multilingual loan recovery process, AI provides the execution force necessary to go infinite and beyond in terms of scale and cost-effectiveness. The Cost of Acquisition (CAC) and Cost to Collect (CTC) get drastically reduced while your human capital starts behaving like advisors instead of mere robotic dialers.