The Great Shift: How AI Voice Bots Are Changing Loan Recovery in NBFCs

Important Points for NBFC Heads:

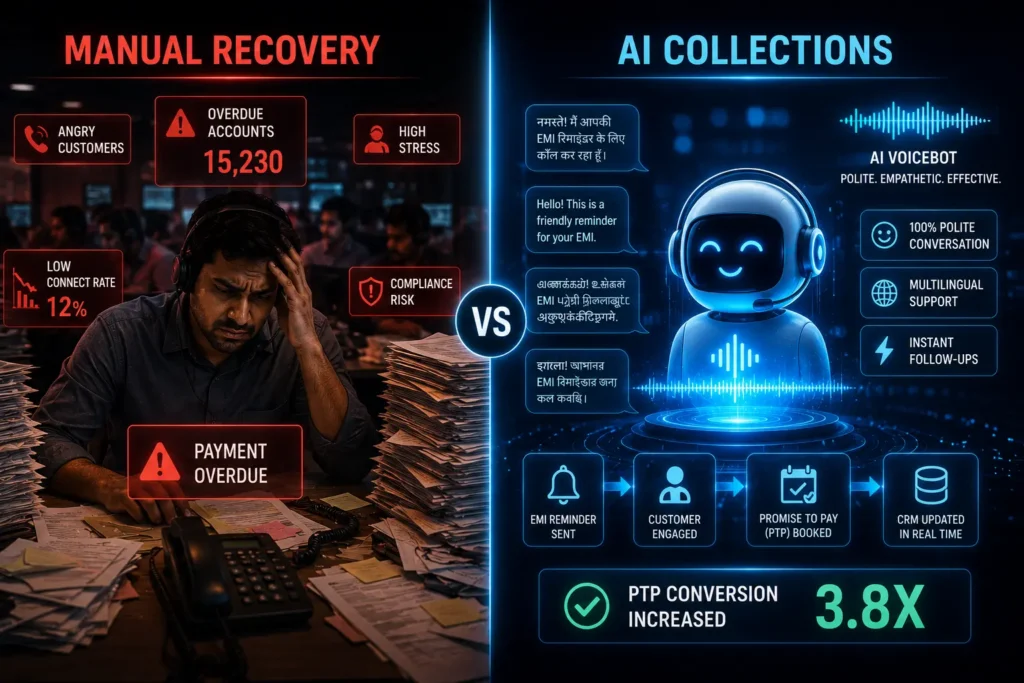

The Manual Problem: Dependence on manual call center agents for early recovery of the disbursed funds is a costly and inefficient strategy that usually poses a great risk to regulatory and branding compliance issues AI Voice Bots Changing Loan Recovery.

AI Transformation: Conversational AI technologies have moved beyond irritating IVRs. Contemporary chatbots comprehend human intentions, agree upon repayment dates, and communicate effortlessly in local dialects.

Empathic Voicebot Benefits: AI-based voicebots don’t feel irritation. They offer friendly, empathic, and 100% compliant reminders, which resulted in a dramatic increase in “Promise to Pay” (PTP) conversions.

Being a head of a Non-Banking Financial Company (NBFC) or overseeing a collections team at a financial firm is among the toughest positions within the industry today. Over the past decade, the process of lending has been transformed from end to end.

It now takes mere seconds to evaluate a borrower, minutes to complete e-KYC, and less than an hour to issue a loan. The reverse process, namely, the collection of money lent out by your company, still remains a tedious task.

In fact, for many years, the conventional method of debt recovery used by NBFCs in India was quite easy but had several flaws – using hundreds, sometimes even thousands, of humans in a massive BPO operation to make repeated calls to non-paying borrowers until they settled the dues.

The time-tested conventional method is now facing its biggest challenge. The growing operational costs, strict RBI regulations on collection processes, and loss of consumer trust has made this process unworkable.

Top NBFCs understand that early debt collections (Bucket 1 and Bucket 2) need not be handled through tough negotiations but should rather involve continuous and systematic reminders to the customer. Here comes the role of Conversational AI Voice Bots.

The Breakdown of the Manual Call Center Model

To see why AI is important, it is imperative to understand why the current manual process is not scaling well enough.

A. The Risks of Compliance and Branding

Debt collection is a very stressful business. Debt collectors are put under tremendous pressure to achieve certain recovery goals every day. After 100 calls of being insulted, rejected, or verbally abused by a debtor, a human debt collector becomes highly irritated and frustrated.

Frustration makes them lose control, start raising their voice and use aggressive tones with a borrower. Under today’s regulations, a single instance of aggression can cost a firm huge fines from the RBI, loss of license, and negative publicity that ruins its reputation forever.

B. The Linear Scalability Problem

If you increase your loan portfolio by 30%, it doesn’t mean that you can add 30% more people to your collections department. Hiring more people means spending more money on payroll, renting more space for offices, buying more software licenses, and training personnel. It means linear scaling, which increases your OPEX.

C. Inconsistent Implementation

The human agent has physical constraints. If there are 15,000 EMIs bounced back on the fifth of the month, the team cannot contact all 15,000 defaulters by noon. There is a delay in follow-up. The borrower may be contacted three days late, by which time their account becomes more delinquent.

Enter Conversational AI: The New Face of Collections

Smart NBFCs are increasingly moving away from the “brute force” approach of dialing calls manually and adopting the Agentic AI Workflows framework.

It is crucial to make a distinction between existing technologies and cutting-edge technologies. This is not about interactive voice response systems where callers have to press keys to do things like pay bills.

This is about advanced conversational AI bots that use natural language processing and machine learning algorithms to communicate seamlessly with borrowers.

Empathy and Infinite Patience at Scale

One of the most baffling things about Artificial Intelligence is how it may provide better “humane” service than the highly-stressed person on the other line.

Imagine that the customer is late on a payment and already stressed out. They answer the call, only to be yelled at by the collector, and they hang up the call or simply choose not to make a payment.

The Archiz Solutions AI Voicebot will always remain calm because it has no ego that can be bruised and no temper to get into trouble. It will collect with 100% politeness, 100% of the time.

The Scenario: “Your EMI of ₹5,000 was due yesterday,” says the AI voice bot. * The Response: The borrower answers, “I am sorry, but I just lost my job, so I do not have the money at the moment.”

The AI Response: Rather than engaging in a pointless argument, the voice bot recognizes the sentiment and provides support: “I understand it must be hard for you right now, but would you like me to schedule a callback next week, or maybe consult you with our financial advisor?”

Such politeness ensures full adherence to the RBI regulation.

Vernacular Power: Winning the "Bharat" Market

When NBFCs venture into Tier 2, Tier 3, and rural India, their biggest challenge becomes that of language. They cannot collect a loan from a farmer in rural Maharashtra in English, which is forced upon them in corporate circles. The trust in finance is established completely in the local language, but it is not feasible from an HR perspective to recruit a BPO with 12 different regional languages.

The AI voicebot addresses the above problem immediately. An AI voicebot can change its language dynamically based on the geographic pin code or CRM details of the borrower.

It will be able to speak fluently in Hindi, Marathi, Tamil, Telugu, Bengali, and several other languages. When borrowers hear someone speak to them in their local language, they have a high probability of cooperating and providing a Promise to Pay (PTP).

Flawless CRM Integration and Data Hygiene

Data loss is one of the biggest flaws with manual collection efforts. For instance, a person may successfully make an appointment with the borrower to repay their loans on Friday; however, forget to enter this date into LMS. Consequently, another person contacts the borrower on Thursday, enraging them.

The AI Voicebots work as a fully-fledged technological layer. When the voicebot communicates with the debtor and makes an agreement regarding when to repay a loan, NLP technology immediately identifies this exact date and enters it into your CRM through webhooks.

Conclusion: The Agentless Future

The future of debt collection will not be about making call centers noisier but rather about making them smarter, more automated, and emotionally intelligent. With the use of AI Voicebots, NBFCs are witnessing cost savings of up to 40% on calling expenses, along with a twofold increase in connection rates.